Discover Latest HMRC R&D Tax Credit Statistics.

The 2024 R&D Tax Credits Statistics were released by HMRC on 26 Sep 2024, revealing significant shifts in the landscape, especially for SMEs.

2024 R&D Tax Credits Statistics

The 2024 R&D Tax Credits Statistics were released by HMRC on 26 September 2024 revealing significant shifts in the landscape, especially for SMEs and larger businesses alike:

1. Decrease in Claim Volume

The total number of R&D tax credit claims has dropped by 21%, down to 65,690 claims from 83,240 the previous year. Notably, SMEs saw the hardest hit, with a 23% decline in claims. This drop is attributed largely to HMRC’s stricter compliance measures, including the introduction of the Additional Information Form (AIF) and pre-notification requirements.

Despite this reduction in claim volume, overall relief remained stable at £7.5 billion, driven by a 26% increase in the average claim value within the SME scheme. This suggests a concentration of larger claims.

Number of claims for R&D tax credits by scheme, 2015 to 2016 tax year to 2022 to 2023 tax year

2. Shift Towards Larger Claims

A notable trend has been the shift towards larger claims, particularly under the Research and Development Expenditure Credit (RDEC) scheme. While the number of claims fell, the average claim size in RDEC rose by 18% to £291,365. This indicates that larger companies are increasingly benefiting from the incentive, while smaller businesses may be struggling with the more complex requirements and could be partly down to the RDEC rate increase from 13% to 20%.

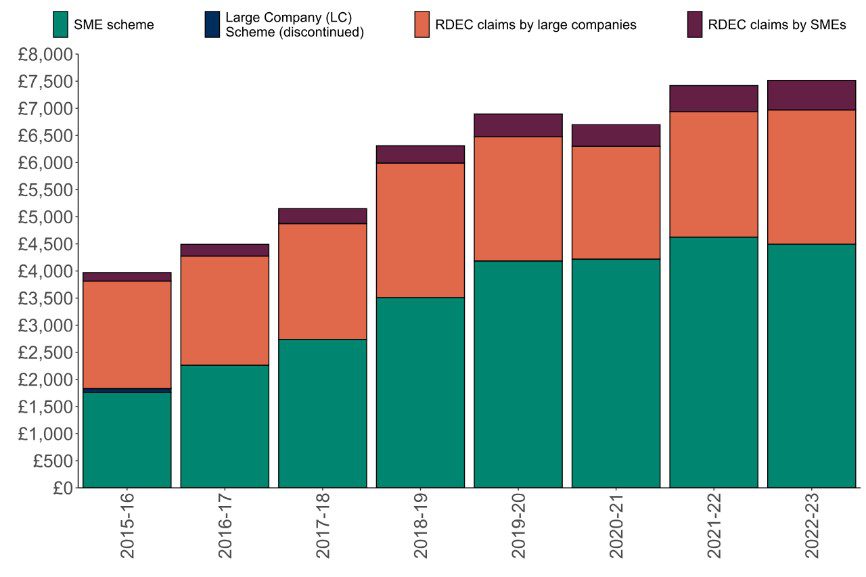

Total support claimed through R&D tax credits by scheme, 2015 to 2016 tax year to 2022 to 2023 tax year (£ million)

R&D expenditure used to claim R&D tax credits by scheme, 2015 to 2016 tax year to 2022 to 2023 tax year (£ million)

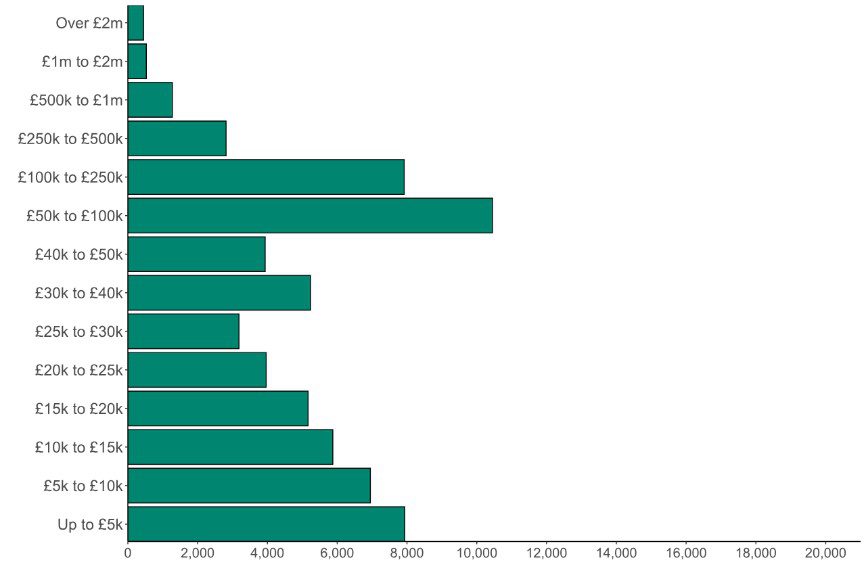

Number of R&D tax credit claims by cost band, 2022 to 2023

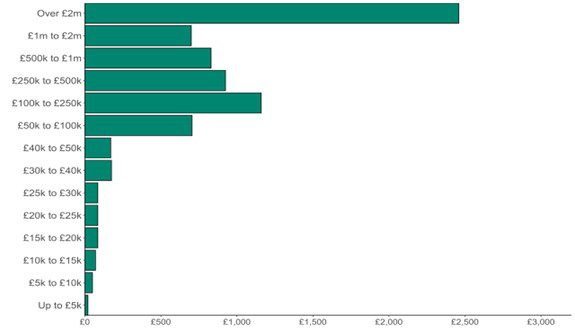

Amount of R&D tax credits claimed by cost band, 2022 to 2023 (£ million)

3. Industry and Regional Breakdown

The Information & Communication, Manufacturing, and Professional, Scientific & Technical sectors remained dominant, accounting for 65% of total relief. London continues to lead regionally, with 23% of total claims and 32% of the relief, but the overall distribution remains consistent across the South East and East of England.

Number and amount of R&D tax credits claimed by region of company registered address, 2022 to 2023 (£ million)

R&D tax credit claims by industry sector, % change between 2021 to 2022 and 2022 to 2023

4. Challenges for First-Time Claimants

One worrying trend is the decline in first-time applicants, down 19% for SMEs. The new compliance requirements, while helping to reduce fraudulent claims, are potentially creating barriers for smaller, innovative companies. It’s crucial that startups and scale-ups receive the support they need to navigate these changes and not be deterred by administrative burdens.

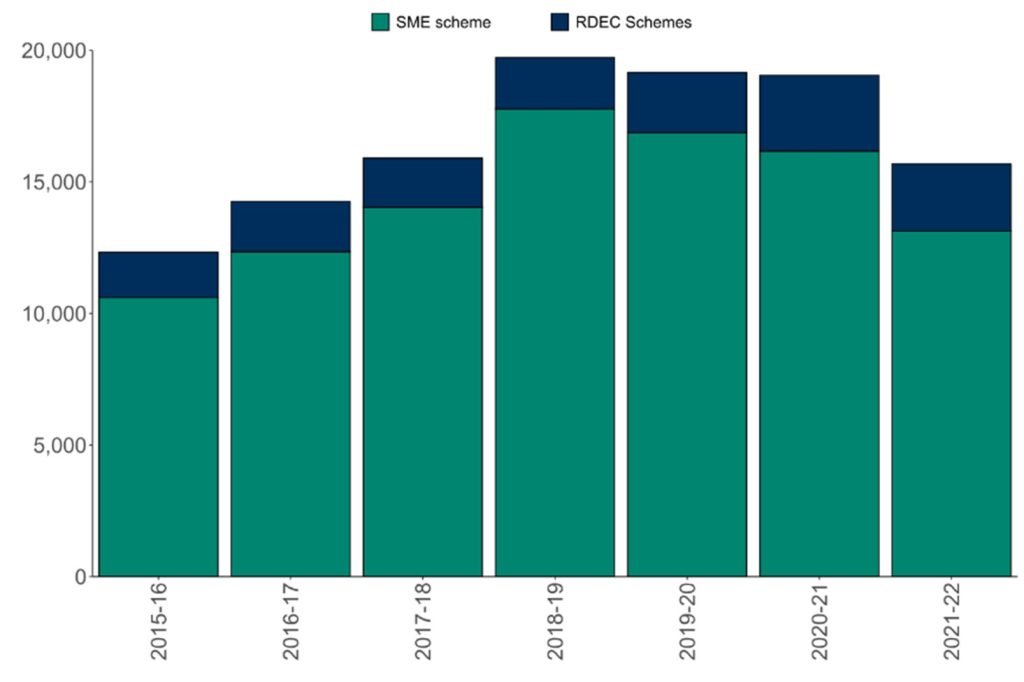

Number of first-time applications by scheme, 2015 to 2016 tax year to 2021 to 2022 tax year

Key Takeaway: While theR&D Tax Reliefsystem remains a valuable incentive for larger companies, SMEs need better guidance and support to overcome the increasing complexity. The rise in claim values shows that genuine R&D is still being rewarded, but we must ensure smaller innovators aren’t left behind. With further reforms expected, businesses should stay informed to maximise their R&D opportunities.

The recent changes in R&D Tax Relief highlight the need for businesses to stay informed and adaptable. As compliance measures become more stringent, the challenge for many companies, especially SMEs, is ensuring they continue to benefit from this crucial incentive. By understanding the evolving landscape, businesses can make informed decisions that will support their innovation efforts and sustain long-term growth.

🔑 Next steps: If your business is involved in R&D, it’s vital to stay ahead of these changes. Engaging with knowledgeable advisors or reviewing your current approach to R&D Tax Credits can help ensure your claims are fully compliant and optimised for the future.

At Innovation Tax, we dedicate time to our clients and partners to inform them of changes and new developments which may be of interest and go over and above expectation to demonstrate that we are not just R&D Tax experts.

Start the conversation with a complimentary, no-obligation chat about your R&D work.

Innovation Tax specialise in helping companies access vital innovation tax incentives and grant funding to enable their businesses to grow, increase profitability, reduce risk and enable further investment in R&D, IP and capital assets.